European Automotive Market 2026: Overview and Segment Analysis

The European automotive market entered 2026 with a slow start. In January, car sales in the EU declined by 3.9% year-over-year, dropping to 799,625 units. However, a recovery began in February, with EU sales increasing by 1.4% to reach 865,437 units.

Across the EU+UK+EFTA region, total sales stood at 961,382 units in January (-3.5% YoY) and 979,321 units in February (+1.7% YoY). Overall, during the first two months of 2026, total EU car sales decreased by approximately 1.2% compared to the same period last year.

Despite the slight contraction in total volume, the share of electric vehicles (BEVs) and hybrid cars continues to grow rapidly. By the end of 2025, BEVs accounted for 17.4% of the EU market, while hybrids reached a significant 34.5% share. In summary, while overall market volume remains relatively stagnant in 2026, the electrification trend continues at full speed.

January–February 2026: Total Sales and Market Changes

- January 2026 (EU): 799,625 units (-3.9% YoY)

- January 2026 (EU+UK+EFTA): 961,382 units (-3.5% YoY)

- February 2026 (EU): 865,437 units (+1.4% YoY)

- February 2026 (EU+UK+EFTA): 979,321 units (+1.7% YoY)

- Jan–Feb 2026 (EU YTD): -1.2% YoY

In January, sharp declines in markets like France weighed heavily on overall performance, while Germany and Italy helped soften the drop. In February, Germany (+3.8%), Italy (+14.0%), and Spain (+7.5%) showed growth, whereas France experienced a significant decline of -14.7%.

These figures highlight not only a slowdown in demand at the start of 2026 but also a highly fragmented market performance across countries.

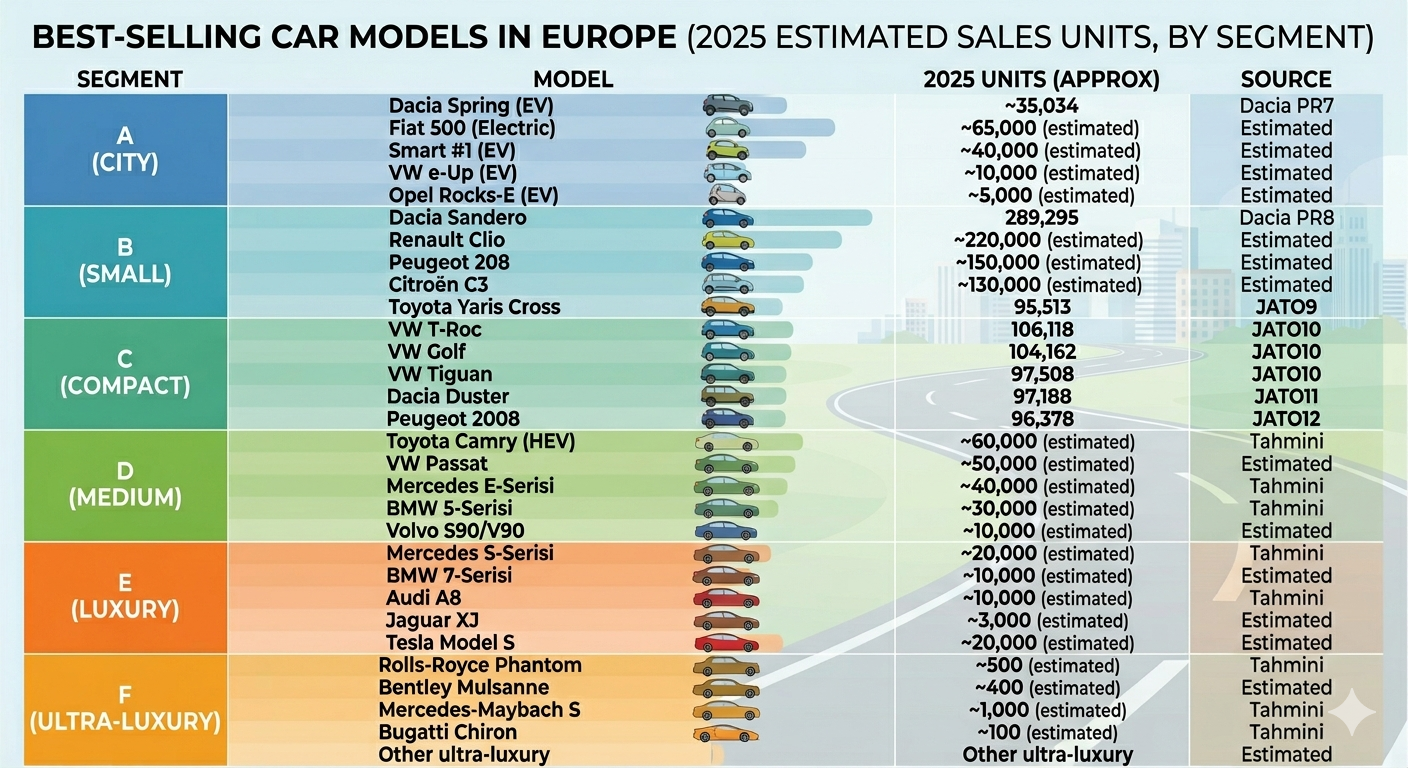

Best-Selling Models by Segment

In Europe, vehicle segments (A–F) show significant variation in both market share and consumer preferences. While electric vehicles dominate the A-segment (city cars), hybrid and internal combustion engine (ICE) models still remain strong in mass-market segments like B and C.

According to 2025 data, the best-selling model in the EU was the Dacia Sandero (B-segment).

Estimated Segment Leaders (2025) - Some figures are estimated due to limited official data availability.

Powertrain Distribution

Electrification is becoming increasingly dominant across the EU market. By the end of 2025, the powertrain distribution was as follows:

- BEV (Battery Electric Vehicles): 17.4%

- Hybrid (HEV): 34.5%

- Plug-in Hybrid (PHEV): 9.4%

- Petrol: 26.6%

- Diesel: 8.9%

In the A-segment, most vehicles are fully electric. In B and C segments, hybrid and alternative fuel options (such as LPG-electric combinations) are widely available.

For example, the Dacia Sandero features a mix of 48% petrol and 52% LPG variants, while models like the Fiat 500 and Smart #1 are fully electric.

Overall, the share of petrol and diesel vehicles continues to decline across all segments, while BEV, HEV, and PHEV adoption is accelerating rapidly. This transformation is particularly evident in major markets such as Germany and France. In 2025, BEV sales in Germany increased by 43%, followed by strong double-digit growth in countries like the Netherlands, Belgium, and France.

Country-Level Sales and Market Share

In 2025, Germany remained the largest automotive market in the EU with 2,857,000 units sold. It was followed by:

- France – 1,632,000 units

- Italy – 1,525,000 units

- Spain – 1,149,000 units

These four countries together account for approximately 50% of total EU car sales.

At the start of 2026, these major markets are showing mixed trends. Germany and Italy are experiencing growth (Germany +3.8% in February), while France is facing a sharp decline (-14.7% in February).

Excluding the UK market, total EU+EFTA sales remained relatively stable compared to the previous year.

Estimated market shares by country (2025):

- Germany: ~25%

- France: ~15%

- Italy: ~14%

- UK: ~10%

Brand Market Shares and Key Players

In 2025, the Volkswagen Group led the European market with 2,988,870 units sold, capturing approximately 27.6% market share.

It was followed by:

- Stellantis Group: 1,660,155 units (15.3%)

- Renault Group: 1,239,693 units (11.5%)

Within the Volkswagen Group, brands such as Volkswagen, Skoda, and Audi played a major role. Meanwhile, Toyota maintained a strong position with around 855,000 units sold.

Chinese brands are rapidly gaining ground in Europe:

- BYD increased its European sales by 165%

- MG reached approximately 300,000 units in 2025 (+30%)

On the other hand, Tesla experienced a 17% decline in sales.

Other notable brands in the EU market include Mercedes-Benz, BMW, Peugeot, and Dacia.

References: Figures compiled from official and reliable sources have been used. Key sources include: European Automobile Manufacturers Association (ACEA) reports, Reuters and other news agencies, Dacia and manufacturer press releases, Bestselling-cars.com data, and Anadolu Agency automotive news. For missing data, reliable industry analyses and estimates have been used (indicated as estimates).